INVESTMENTS

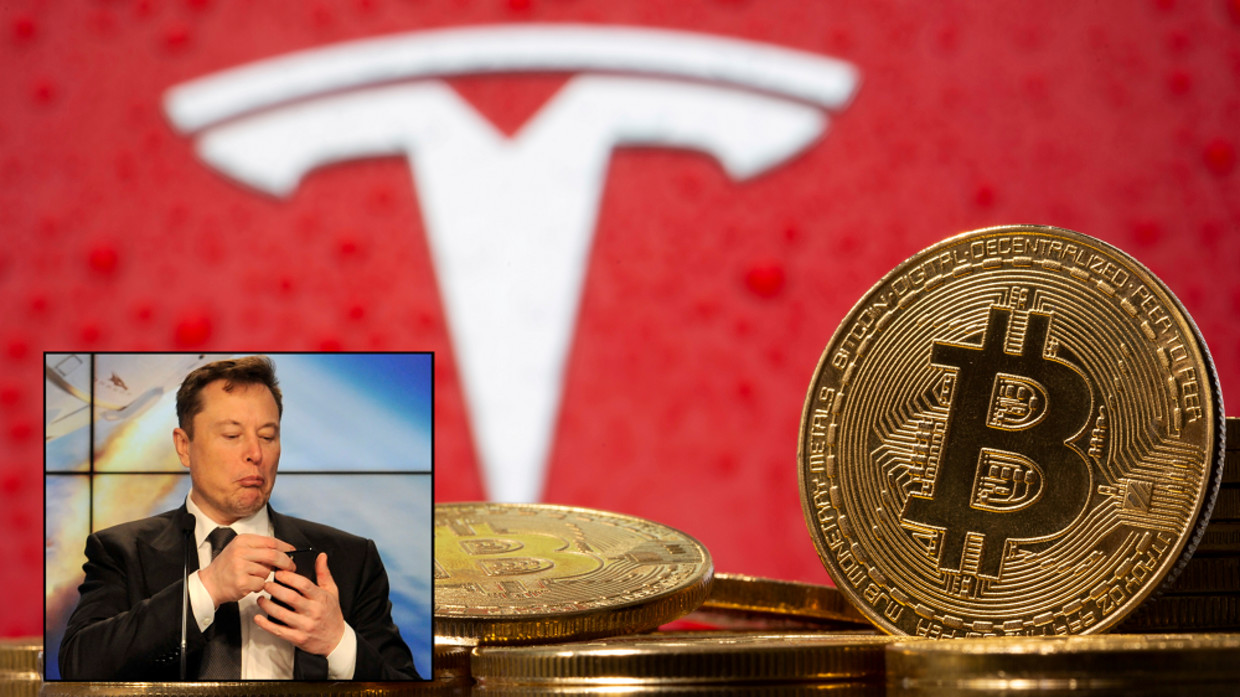

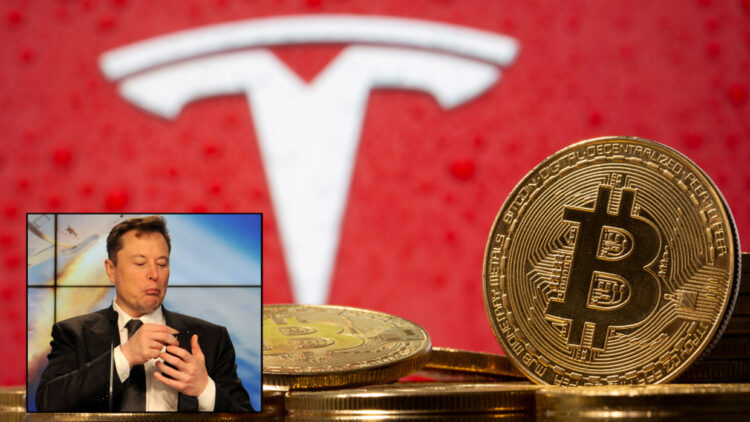

Musk says Tesla SUSPENDING Bitcoin use, citing environmental impact

Tesla CEO Elon Musk has announced he will stop taking Bitcoin for vehicle purchases or selling the cryptocurrency until mining procedures transition to “more sustainable energy” than coal or fossil fuels.

“We are concerned about rapidly increasing use of fossil fuels for Bitcoin mining and transactions, especially coal, which has the worst emissions of any fuel,” Musk tweeted on Wednesday evening.

Cryptocurrency is a good idea on many levels and we believe it has a promising future, but this cannot come at great cost to the environment.

Tesla & Bitcoin pic.twitter.com/YSswJmVZhP

— Elon Musk (@elonmusk) May 12, 2021

Tesla doesn’t intend to sell any of the Bitcoin it currently holds, however, but will hold on to it until “mining transitions to more sustainable energy,” and is looking at other cryptocurrencies that use “<1% of Bitcoin’s energy/transaction.”

That last metric might be a hint Musk is considering Dogecoin, a meme currency he recently embraced – and even hawked on Saturday Night Live in his guest host appearance last weekend.

Do you want Tesla to accept Doge?

— Elon Musk (@elonmusk) May 11, 2021

The about-face comes less than two months after Musk announced that Tesla would be accepting Bitcoin as payment for vehicles, having bought an estimated $1.5 billion worth of Bitcoin by late March.

‘It’s a hustle’: Elon Musk DESTROYS Dogecoin as he brings crypto memes to his episode of SNL

Bitcoin’s price plummeted after Musk’s tweet, going from $54,602 to 52,467 within just ten minutes before recovering slightly – and leading to speculation that the Tesla and SpaceX boss was trying to drive the price down before buying up some more.

Bitcoin mining is energy-intense – in March 2021 it was estimated at 129 terawatt hours, more than enough to power Norway for a year. Few if any studies have been done on crypto mining’s carbon footprint, with Musk presumably extrapolating it from the percentage of total electricity generated by oil, gas and coal – rather than wind, water, solar or nuclear power.

On Monday, Musk announced he would launch a satellite to the lunar orbit next year named Doge-1 and funded entirely by Dogecoin, meaning that “to the moon” memes were literal, and not referring to Dogecoin’s rapidly rising value – which dropped substantially after Musk’s attempt at comedy.

Not another SNL skit? SpaceX to launch DOGE-1 satellite TO THE MOON in 2022, Elon Musk says

Think your friends would be interested? Share this story!

- The precious metal has rallied ahead of an expected interest rate cut by the US Federal Reserve

- The price of gold reached an all-time high on Friday, soaring above $2,600 per ounce as global investors continue to seek safe-haven assets.

Spot gold prices rose 1.13% to a record high of $2,609.8 per ounce before pairing some gains. Prices were up roughly 4% for the week and 23% so far this year, exceeding the 13% advance registered for all of 2023.

Gold has rallied after reports last week that the US Federal Reserve might be ready to lower rates by 50 basis points next week from the current 5.25% to 5.50%, the highest level since 2001. Lower borrowing costs increase the appeal of non-yielding gold.

Analysts attribute the rally to investor demand for safe-haven assets amid global uncertainty and rising geopolitical tensions in the Middle East and Eastern Europe.

Investors traditionally turn to gold in times of market uncertainty to hedge risks and as a store of value. For thousands of years, bullion has been seen as a safe haven during periods of economic instability, stock market crises, military conflicts, and pandemics.

The price of gold has also been buoyed by the dollar’s weakness. The greenback has fallen to the lowest level this year against a basket of peer currencies ahead of the anticipated interest rate cuts by the Federal Reserve.

Bank of America predicted earlier this month that gold prices could go up to $3,000 per ounce within the next 12-18 months.

Other precious metals were also on the rise on Friday, with platinum gaining 2.36% to above $1000 per ounce. Silver went up 3.3% to above $31.

Israeli president comments on Lebanon pager attacks

German central bank issues warning on economy

China is raising its retirement age, now among the youngest in the world’s major economies

Gold price soars to all-time high

Russia warns NATO of ‘direct war’ over Ukraine

In Spotify, music listens to you: streaming platform wins patent to surveil users’ emotions to recommend music

How much YouTube pays for 1 million views, according to creators

Pentagon well aware of Ukraine’s corruption problem

Most Americans want to move on from Biden and Trump – poll

Finland officially joins NATO

Turkish minister escapes fire blast (VIDEO)

Trump savages pop star’s Super Bowl performance

Alec Baldwin sued by Ukrainian family of slain cinematographer

Duran Duran stumbles, Dolly Parton rolls into Rock Hall

Sweden probes possible plot behind Russian pipeline leaks

-

NEWS4 months ago

NEWS4 months agoChina makes its move in Africa. Should the West be worried?

-

NEWS4 months ago

NEWS4 months agoChina is raising its retirement age, now among the youngest in the world’s major economies

-

NEWS4 months ago

NEWS4 months agoRussia warns NATO of ‘direct war’ over Ukraine

-

WAR4 months ago

WAR4 months agoIsraeli president comments on Lebanon pager attacks

-

FINANCE4 months ago

FINANCE4 months agoGerman central bank issues warning on economy

-

INVESTMENTS4 months ago

INVESTMENTS4 months agoGold price soars to all-time high

-

FINANCE4 months ago

FINANCE4 months agoThousands of EU automotive jobs at risk