INVESTMENTS

Trading app Robinhood accused of AUTOMATICALLY SELLING users’ shares after banning GameStop stock – reports

After forbidding its users from buying several volatile stocks, including shares in GameStop, trading app Robinhood was allegedly caught selling its users’ stocks against their will, and in doing so hammering down their value.

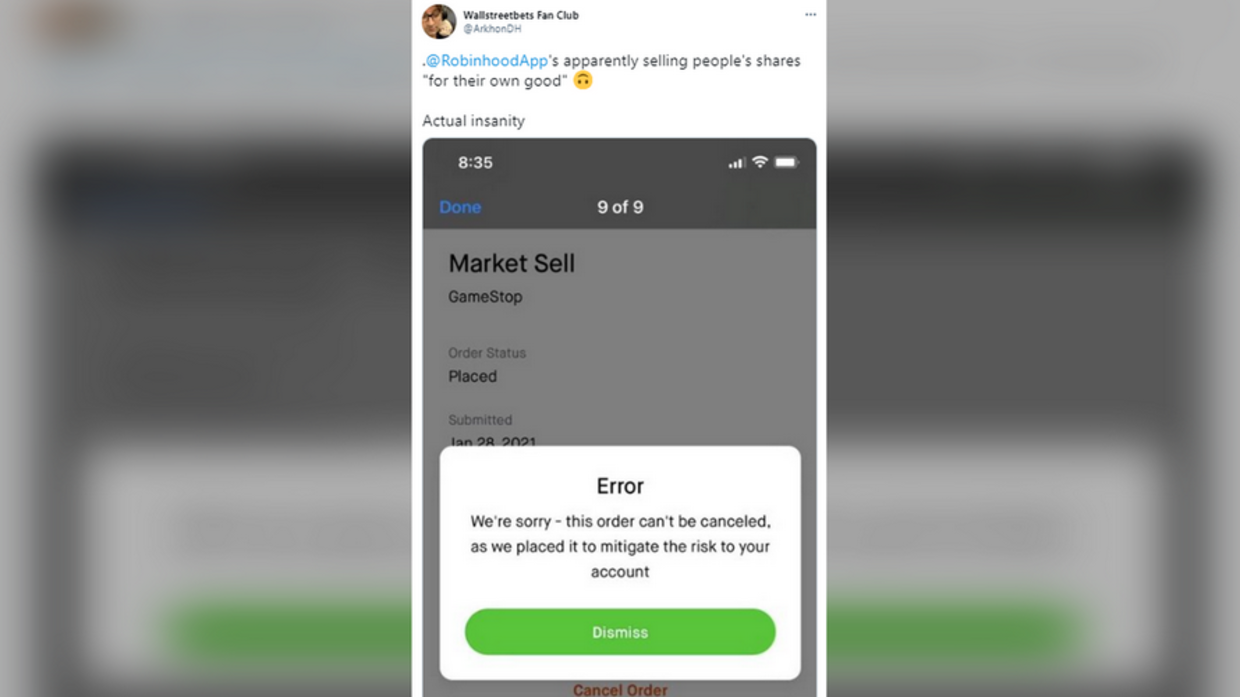

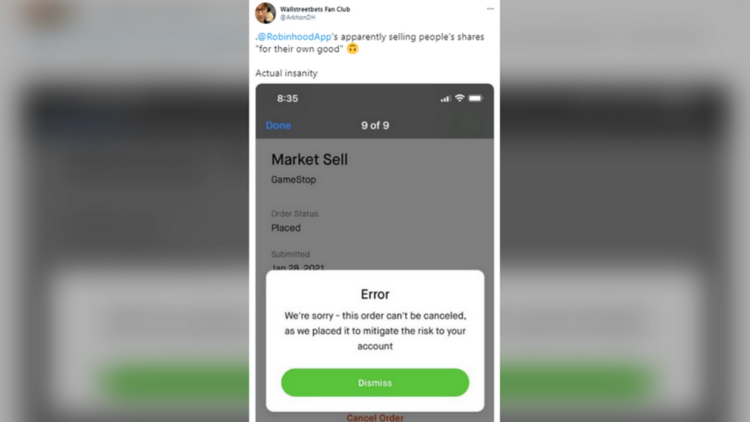

Twitter users on Thursday reported seeing their GameStop shares sold and their positions closed, with Robinhood justifying the sale due to “unreasonable risk.”

Robinhood literally closing out positions against the user's will in $GME.

I'm sure they have something in their ToS about this, but wow. pic.twitter.com/M0juagPLfB

— J◎e McCann (@joemccann) January 28, 2021

Traders who attempted to cancel the sale were met with a message telling them the sale couldn’t be undone, “as we placed it to mitigate the risk to your account.”

Earlier in the day, Robinhood banned the buying of $GME, $AMC, $BB and $NOK (GameStop, AMC Theaters, Blackberry and Nokia) stocks, after small-time traders snapped them up, inflated their value, and got rich while inflicting devastating losses on Wall Street hedge funds, who had gambled a fortune on these companies’ decline.

Robinhood trading app accused of MARKET MANIPULATION after GameStop trading shut down

Robinhood’s users were outraged and accused the company of “market manipulation,” but even after a class action lawsuit was filed against Robinhood, the app’s team seemingly went a step further and began selling its users’ shares without their consent.

https://twitter.com/WokeCapital/status/1354864012413063173?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E1354864012413063173%7Ctwgr%5E%7Ctwcon%5Es1_&ref_url=https%3A%2F%2Fwww.rt.com%2Fusa%2F513968-robinhood-gamestop-force-sale%2F

The alleged forced sales came after many of the amateur traders who drove GameStop’s share value from around $18 in December to more than $450 on Thursday morning refused to sell of their own accord.

Had they sold when Robinhood banned buying, the market would have become flooded with shares that would have decreased in value, given fewer customers would have been able to buy them.

https://twitter.com/MarkDice/status/1354877508936552448?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E1354877508936552448%7Ctwgr%5E%7Ctwcon%5Es1_&ref_url=https%3A%2F%2Fwww.rt.com%2Fusa%2F513968-robinhood-gamestop-force-sale%2F

The forced sales apparently had the same effect. GameStop’s stock price rallied from around $240 before users started receiving the notifications to $430 as the apparent sell-off began, before plummeting back to around $220 afterwards. At time of writing, Robinhood had not officially acknowledged the reported automatic sales.

The lower the value of the stocks in question, the less money short-selling hedge funds lose when they buy back the shares they originally borrowed. Online, commentators have accused Robinhood of doing the bidding of Citadel Securities, a Chicago-based firm that handles a majority of the app’s trades and also bailed out Melvin Capital, a hedge fund brought to the brink of bankruptcy by the GameStop surge.

Mega-investors punished with $70 BILLION LOSSES as GameStop and other shorted firms see stock surge – data analysts

Across the board, the financial establishment has reacted with outrage to the surge in what previously were considered dead stocks. Industry insiders have taken to TV to decry the amateur investors, hedge fund billionaires have demanded the government intervene on their behalf, and investment firms have bailed out their short-selling colleagues who lost tens of billions of dollars when the stocks rose, instead of falling as they predicted.

Wall Street’s fury, however, has united multiple sides of the political compass in defiance. Democratic congresswomen Rashida Tlaib and Alexandria Ocasio-Cortez of the progressive ‘squad’ have called for Congressional hearings into Robinhood’s alleged “manipulation.”

Texas Republican Ted Cruz has also lent his support, while eccentric billionaire Elon Musk – an early advocate for the amateur traders – responded “absolutely” to Ocasio-Cortez’s calls for investigation.

This is unacceptable.

We now need to know more about @RobinhoodApp’s decision to block retail investors from purchasing stock while hedge funds are freely able to trade the stock as they see fit.

As a member of the Financial Services Cmte, I’d support a hearing if necessary. https://t.co/4Qyrolgzyt

— Alexandria Ocasio-Cortez (@AOC) January 28, 2021

When @AOC and @DonaldJTrumpJr are on the same side you know you fucked up @RobinhoodApp pic.twitter.com/y15FBqrUu9

— Dave Portnoy (@stoolpresidente) January 28, 2021

White House Press Secretary Jen Psaki said on Wednesday that Treasury Secretary Janet Yellen was “monitoring the situation.”

However, Yellen has taken more than $800,000 in ‘speaking fees’ from Citadel. Asked on Thursday whether Yellen would recuse herself from advising President Joe Biden on the situation, Psaki did not answer yes or no, stating instead that Yellen is “one of the world-renowned experts on markets, on the economy,” and that “it shouldn’t be a surprise to anyone she was paid to give her perspective and advice before she came into office.”

- The precious metal has rallied ahead of an expected interest rate cut by the US Federal Reserve

- The price of gold reached an all-time high on Friday, soaring above $2,600 per ounce as global investors continue to seek safe-haven assets.

Spot gold prices rose 1.13% to a record high of $2,609.8 per ounce before pairing some gains. Prices were up roughly 4% for the week and 23% so far this year, exceeding the 13% advance registered for all of 2023.

Gold has rallied after reports last week that the US Federal Reserve might be ready to lower rates by 50 basis points next week from the current 5.25% to 5.50%, the highest level since 2001. Lower borrowing costs increase the appeal of non-yielding gold.

Analysts attribute the rally to investor demand for safe-haven assets amid global uncertainty and rising geopolitical tensions in the Middle East and Eastern Europe.

Investors traditionally turn to gold in times of market uncertainty to hedge risks and as a store of value. For thousands of years, bullion has been seen as a safe haven during periods of economic instability, stock market crises, military conflicts, and pandemics.

The price of gold has also been buoyed by the dollar’s weakness. The greenback has fallen to the lowest level this year against a basket of peer currencies ahead of the anticipated interest rate cuts by the Federal Reserve.

Bank of America predicted earlier this month that gold prices could go up to $3,000 per ounce within the next 12-18 months.

Other precious metals were also on the rise on Friday, with platinum gaining 2.36% to above $1000 per ounce. Silver went up 3.3% to above $31.

Israeli president comments on Lebanon pager attacks

German central bank issues warning on economy

China is raising its retirement age, now among the youngest in the world’s major economies

Gold price soars to all-time high

Russia warns NATO of ‘direct war’ over Ukraine

In Spotify, music listens to you: streaming platform wins patent to surveil users’ emotions to recommend music

How much YouTube pays for 1 million views, according to creators

Pentagon well aware of Ukraine’s corruption problem

Most Americans want to move on from Biden and Trump – poll

Finland officially joins NATO

Turkish minister escapes fire blast (VIDEO)

Trump savages pop star’s Super Bowl performance

Alec Baldwin sued by Ukrainian family of slain cinematographer

Duran Duran stumbles, Dolly Parton rolls into Rock Hall

Sweden probes possible plot behind Russian pipeline leaks

-

NEWS5 months ago

NEWS5 months agoChina makes its move in Africa. Should the West be worried?

-

NEWS5 months ago

NEWS5 months agoChina is raising its retirement age, now among the youngest in the world’s major economies

-

NEWS5 months ago

NEWS5 months agoRussia warns NATO of ‘direct war’ over Ukraine

-

WAR5 months ago

WAR5 months agoIsraeli president comments on Lebanon pager attacks

-

FINANCE5 months ago

FINANCE5 months agoGerman central bank issues warning on economy

-

INVESTMENTS5 months ago

INVESTMENTS5 months agoGold price soars to all-time high

-

FINANCE5 months ago

FINANCE5 months agoThousands of EU automotive jobs at risk